{kind=link}

After almost two years of a inventory market that appeared to maneuver increased every day, buyers at the moment are experiencing a bout of volatility that has not been seen in fairly a while. So, will the second half of 2022 convey a return to the lackluster market setting that buyers grew accustomed to in 2020–2021 (except for the novel coronavirus sell-off)? Or ought to we anticipate elevated volatility to turn into the norm transferring ahead?

What’s Modified?

Earlier than we reply these questions, let’s assess what’s modified out there and the financial system in such a short while. Getting into 2022, danger property (together with world equities) offered off dramatically on the heels of a stunning transfer increased in inflationary information. Costs for items and providers rose sharply as shoppers emerged en masse from Covid-19 lockdowns, desirous to resume their pre-pandemic spending and journey habits. Quick-forward to the center of the 12 months and an above-average inflation pattern has been exacerbated by rising power costs, tight labor markets, and provide chain disruptions—elevating the price of every little thing from child formulation to used vehicles. Russia’s invasion of Ukraine has additional prolonged the period—and implications—of the elevated inflationary backdrop for buyers.

Notably, sustained inflationary pressures precipitated the Fed to hike rates of interest, which have moved abruptly increased up to now in 2022. Some readers could (accurately) assume that rising charges are extra impactful to mounted revenue investments. Whereas there’s definitely some validity to that sentiment, as evidenced by the very actual carnage felt in mounted revenue markets year-to-date, fairness buyers are usually not fully proof against the hostile results of the Fed’s financial insurance policies. For fairness buyers, during times of rising rates of interest coupled with inflation will increase, the market will usually low cost future money flows at the next rate of interest. Finally, the upper the low cost fee utilized to earnings, the decrease the worth of equities.

The place Do We Go from Right here?

Fairness and glued revenue buyers have skilled declining costs over the previous six months. However the important thing query transferring ahead is, the place can we go from right here? From my perspective, I imagine that inflation is prone to stay elevated for the foreseeable future earlier than abating as we get nearer to the tip of the 12 months. Whereas power and meals costs will probably stay unstable, we’re beginning to see different elements of inflation soften (e.g., housing and labor), which may lead to a extra benign inflationary outlook as we get near the fourth quarter of 2022.

The general view for fairness markets is that elevated volatility must be anticipated through the summer time and into the autumn because the market digests rate of interest coverage and assesses the Fed’s capability to generate a comfortable touchdown for the financial system. That backdrop must be constructive for long-term buyers who want to allocate capital in fairness markets. What sectors, kinds, and market caps must be favored is one other attention-grabbing query, because the disparity in returns has been vital throughout the board to date in 2022.

Worth or Development?

Development-oriented sectors have skilled a notable pullback as of late, largely attributed to the mix of rising charges and extreme valuations. An extra issue is the pandemic’s acceleration of demand for growth-oriented firms, which now face the aftermath of a “pull-forward” impact, as evidenced by latest slowing demand. Some pockets of this progress have resulted in destructive returns paying homage to the dot-com crash of the early 2000s.

What’s very completely different this time round, nevertheless, is the dearth of client and company leverage within the system, coupled with the truth that many of those shares are producing constructive earnings and money flows for buyers. Additional, we imagine that there are various longer-term secular developments in place, reminiscent of developments in medical sciences, a rising world reliance on digitization, and a transition to a extra service-based financial system—which ought to translate right into a extra constructive panorama for growth-oriented buyers transferring ahead.

Regardless of progress’s latest pullback, the backdrop for value-oriented shares stays constructive, even after notable outperformance in latest months. The present financial setting is constructive for worth sectors like financials and industrials, and it’s troublesome to examine that dynamic materially altering within the close to time period. Plus, so long as oil costs stay firmly above $100, there’s apparent help for the earnings prospects for a lot of shares within the power sector.

We imagine that U.S. fairness valuations are comparatively enticing at this level, if earnings don’t disappoint within the second half of the 12 months. When placing new capital to work, buyers could contemplate using a dollar-cost averaging method within the present setting (a method I’ll personally be trying into over the approaching months). Whereas nobody has a crystal ball that may predict whether or not we’ve already seen the lows in markets this 12 months, buyers could take a degree of consolation within the long-term outlook for U.S. equities at present ranges.

Is There a Case for Overseas Equities?

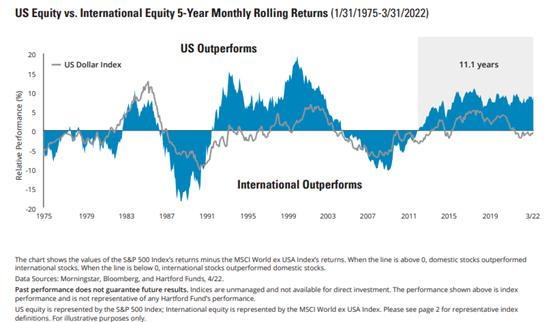

Developed worldwide and rising markets equities have underperformed U.S. equities for a chronic time frame, as evidenced by the chart under. In reality, the outperformance cycle for U.S. equities versus worldwide has lasted a median of seven.9 years since 1975, in response to information from Morningstar and Bloomberg. Slowing financial progress, provide chain disruptions, a powerful U.S. greenback, and heightened geopolitical dangers have all served as headwinds for worldwide equities throughout this era.

Whereas investor sentiment is understandably fairly poor in mild of the efficiency disparity with U.S. equities, is the U.S. versus worldwide dynamic setting the stage for extra enticing relative returns in worldwide markets transferring ahead? Sentiment generally is a highly effective contrarian indicator, so I believe it is sensible to have a wholesome respect for the truth that markets can rally when investor attitudes are, actually, pessimistic.

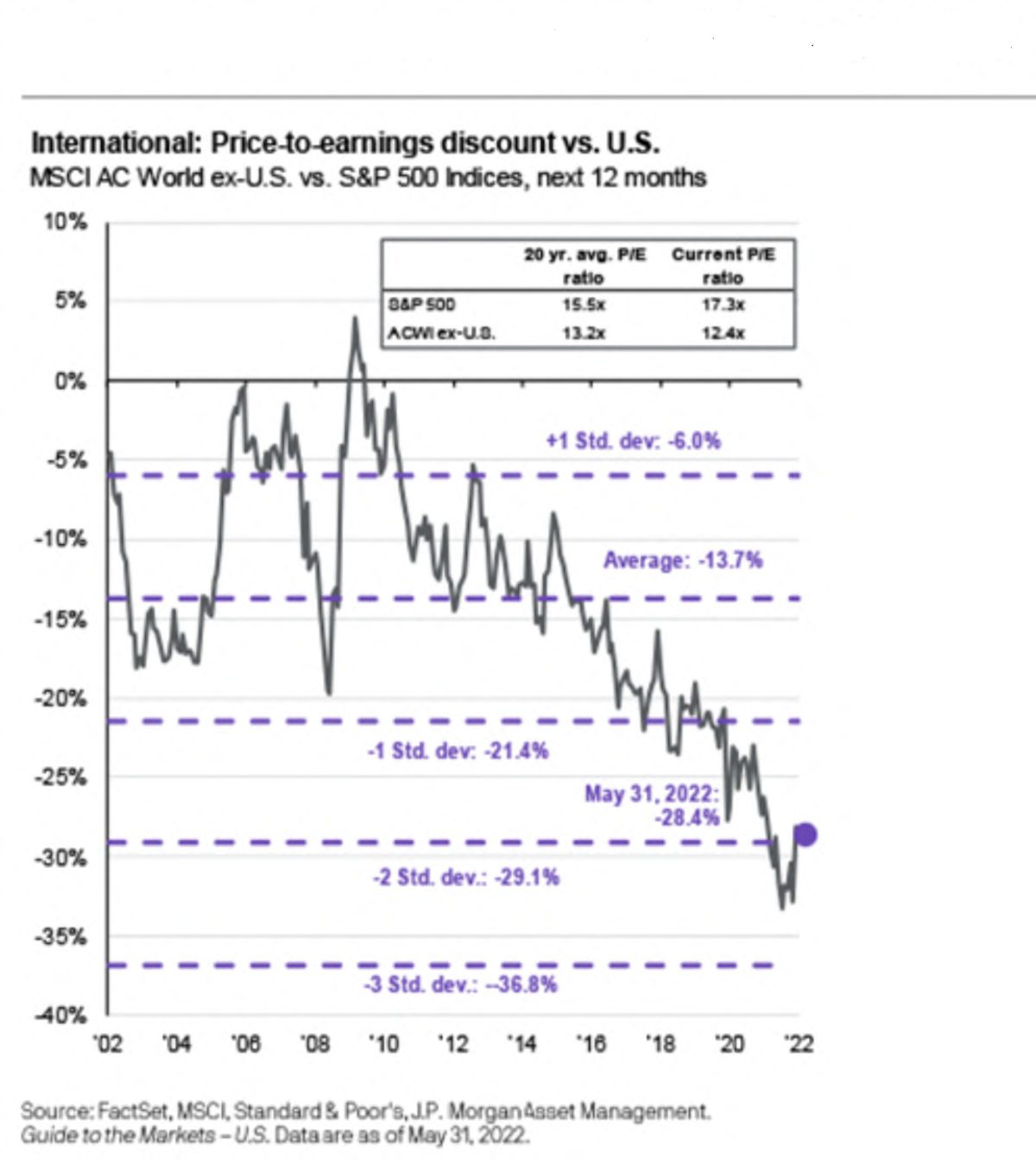

One other issue supporting the forward-looking case for worldwide equities is valuations. The MSCI ACWI ex USA Index was buying and selling at a price-to-earnings (P/E) ratio of 12.4x as of Might 31, 2022, which is under the 20-year common of 13.2x. The notable disparity in valuations between the U.S. and developed overseas equities is highlighted within the chart under.

The bear case for overseas equities within the close to time period, nevertheless, is that fundamentals are prone to stay difficult attributable to heightened geopolitical dangers and till we begin to see constructive developments with the struggle in Ukraine emerge. Within the close to time period, it’s affordable to anticipate that overseas equities could battle to outperform within the present setting.

A Tough Needle to Thread

With no scarcity of near-term challenges for danger property, and equities specifically, buyers are prone to expertise spurts of volatility over the following few months. The market will proceed to judge the Fed’s capability to convey inflation underneath management with out triggering a recession—a troublesome needle to string, although one that’s definitely doable. If profitable, I imagine the stage is about for enticing risk-adjusted returns for fairness buyers over the following three to 5 years.

Greenback-cost averaging is the observe of investing a hard and fast greenback quantity regularly, whatever the share value. Markets will fluctuate, and shoppers should contemplate their capability to proceed investing during times of low value ranges.

The MSCI ACWI ex USA is a free float-adjusted market capitalization-weighted index that’s designed to measure the fairness market efficiency of developed and rising markets. It doesn’t embody the U.S.