{kind=link}

Politicians don’t management the inventory market.

When shares go up presidents get an excessive amount of credit score and once they go down they get an excessive amount of blame. It’s largely circumstantial relying on the timing of cycles and such.

However the markets transfer quicker than ever lately. Traders are consistently pricing sooner or later, typically proper, typically incorrect, but by no means unsure.

The inventory market was already up massive heading into the election however issues took off within the days following the end result.1

Many buyers are positioning for a increase beneath a Trump presidency. The most important pushback I’ve seen is that valuations have been stretched after the massive run-up because the 2022 bear market.

We’ve been in a bull marketplace for a while now. The inventory market must be costly! Let’s have a look at the numbers to see the place issues stand.

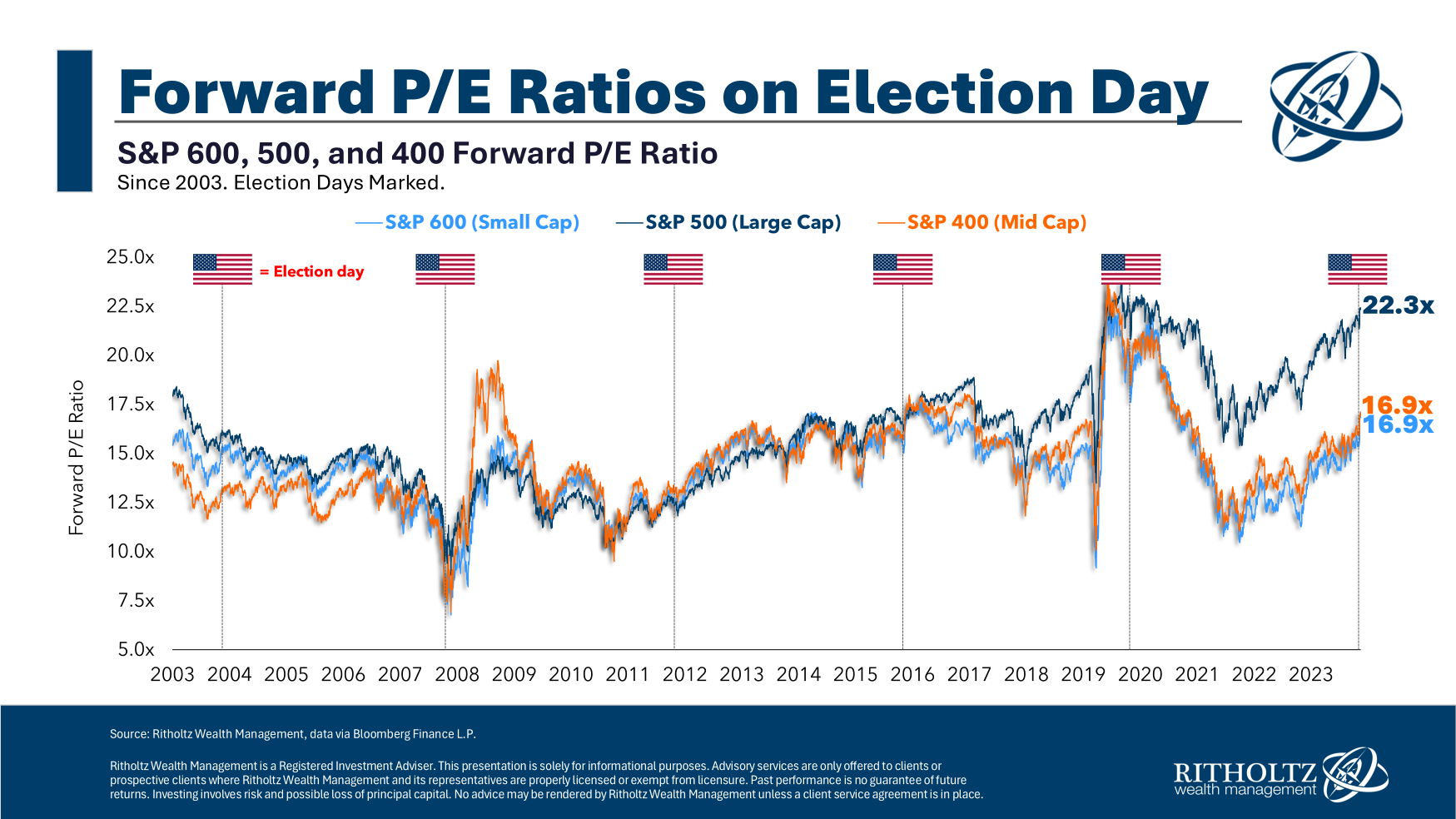

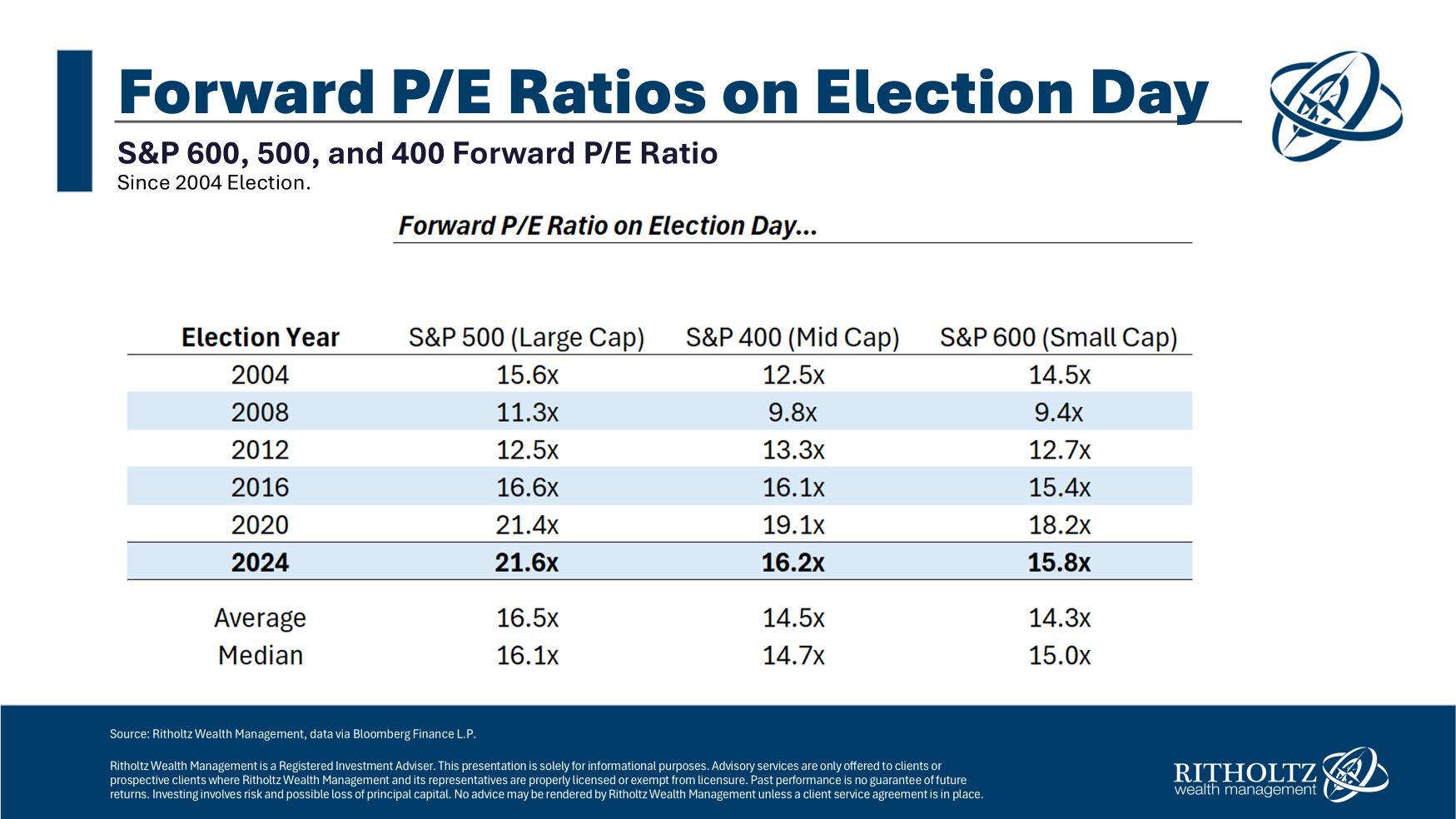

Our crack analysis group seemed again at ahead price-to-earnings ratios on election day for every of the previous six presidential elections:

Listed here are the precise values:

Shares had been clearly less expensive in 2004, 2008 and 2012 as a result of the market was in or popping out of a crash in every of these situations.

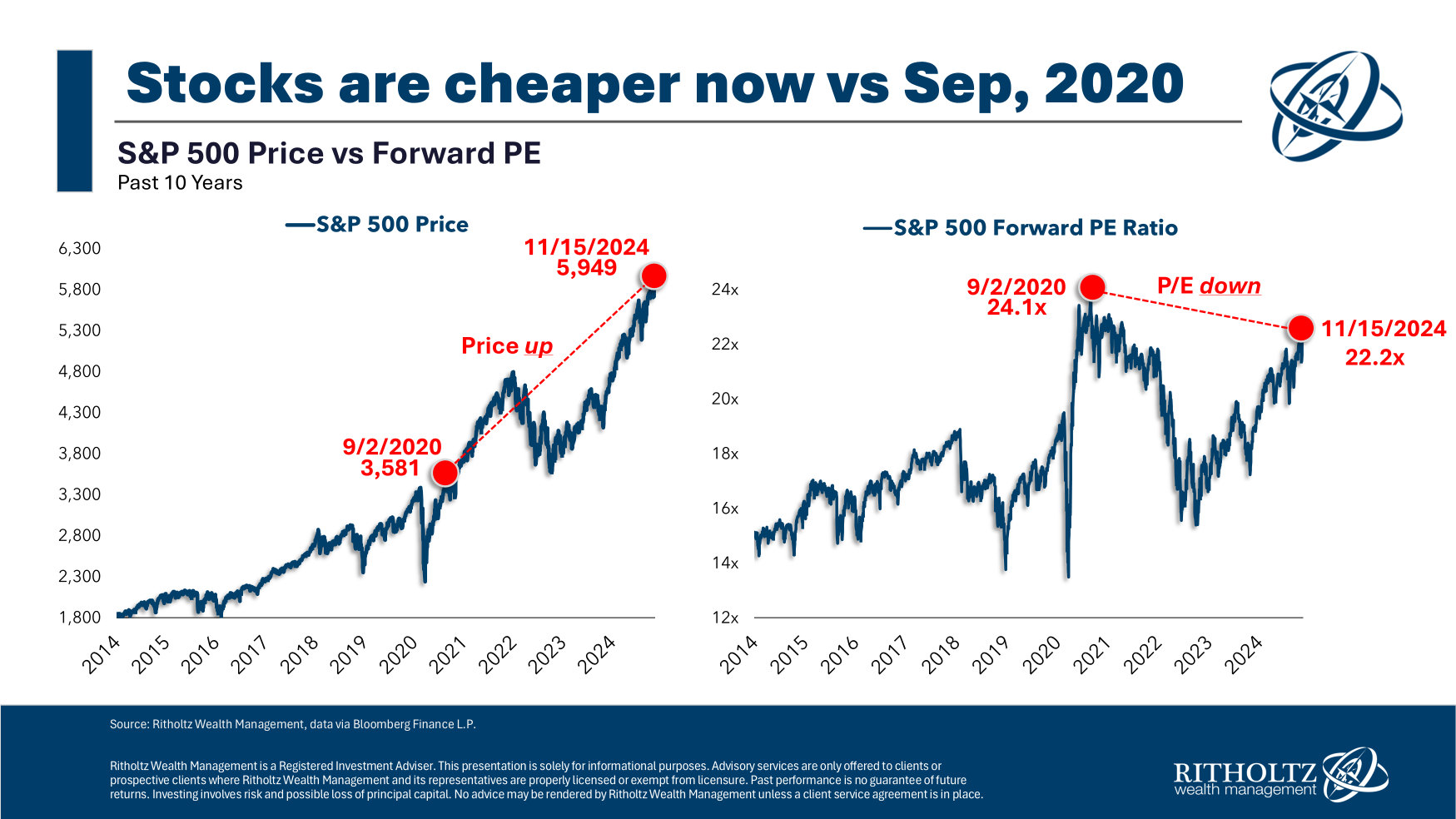

Now have a look at the 2020 and 2024 valuations. The S&P 500 is up almost 90% since election day 2020 but valuations are basically equivalent.

How can that be?

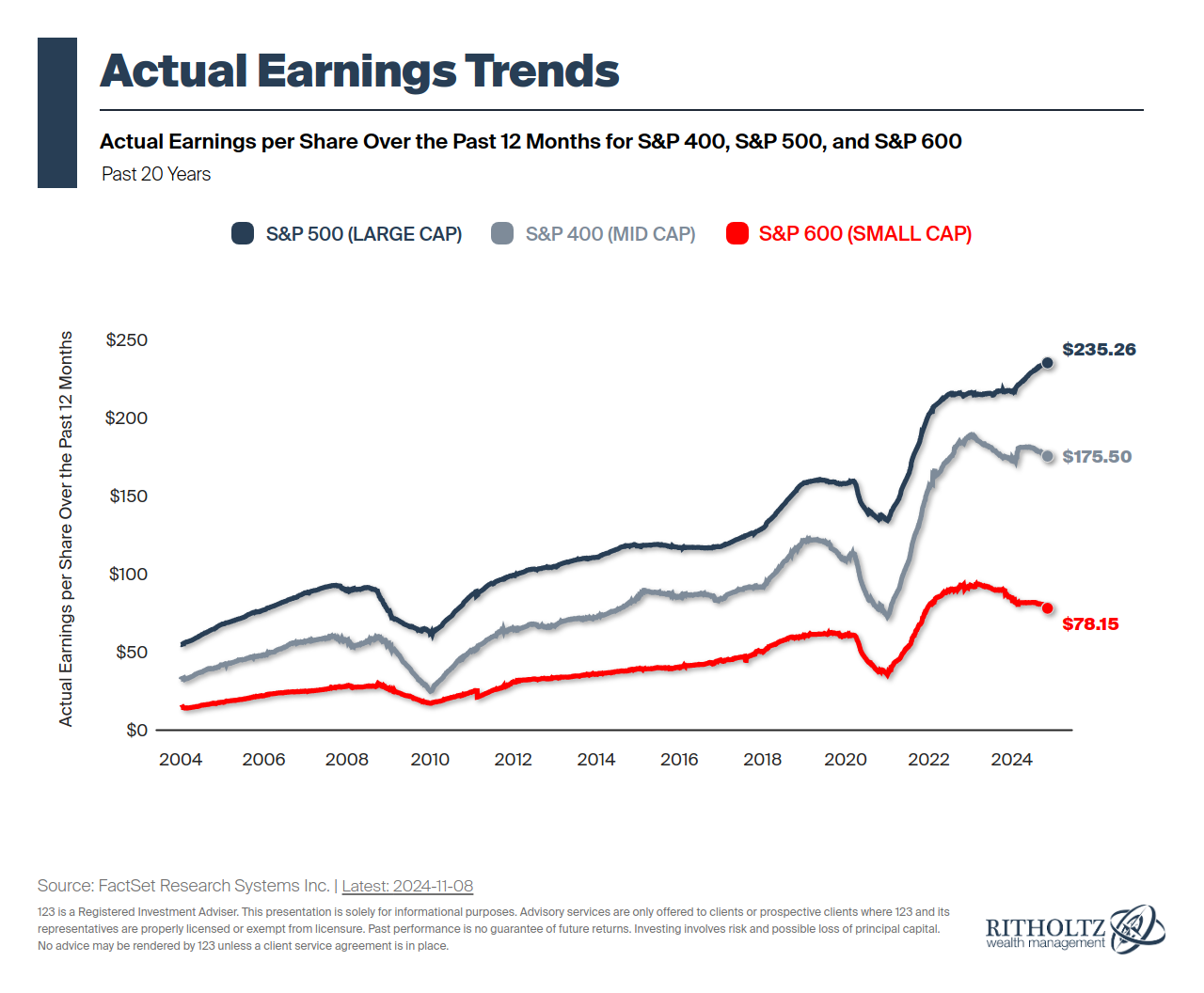

Check out earnings:

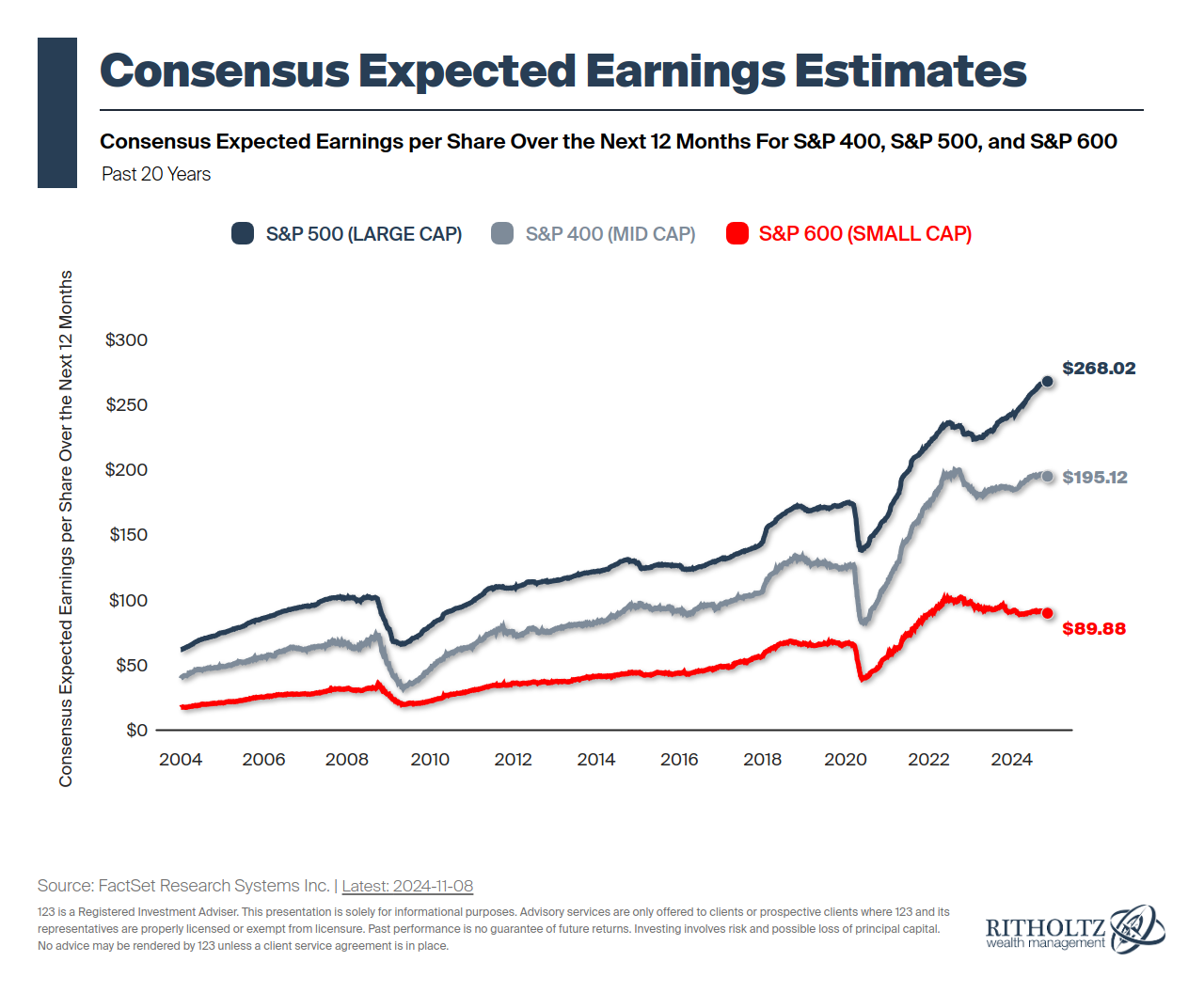

Inventory costs are up quite a bit however fundamentals2 have stored tempo. The truth is, the inventory market has truly gotten cheaper over the previous couple of years due to earnings progress:

Earnings are anticipated to continue to grow too:

In fact, analysts can’t predict the longer term. They could possibly be incorrect however it’s not as unhealthy as some folks would have you ever consider.

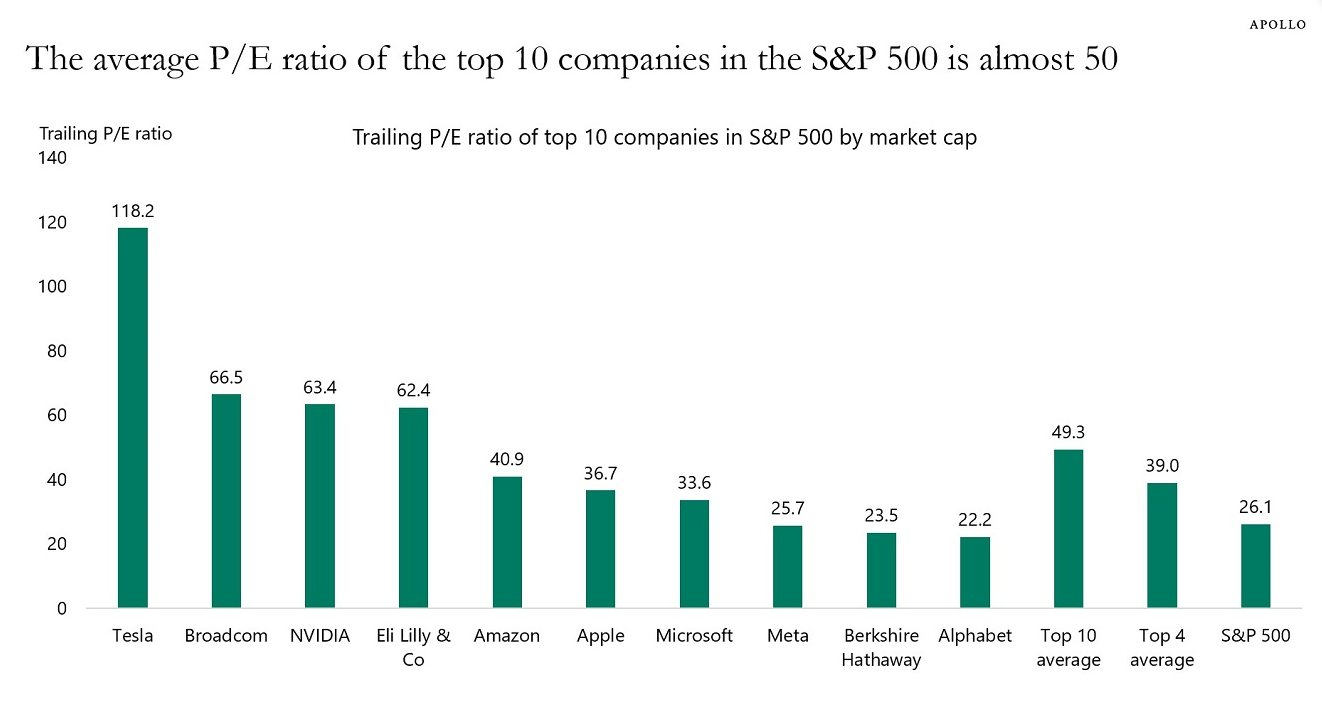

It’s additionally necessary to level out that a lot of the valuation premium on the S&P 500 comes from the most important shares (by way of Torsten Slok):

These shares have excessive valuations for good cause — they’re a few of the best-run firms on this planet.

After I converse to buyers lately there are two extremes on the subject of eager about massive cap U.S. shares:

- The S&P 500 is overvalued. I’m nervous.

- The S&P 500 is the one recreation on the town. Why would I spend money on the rest?

The excellent news for valuation-conscious buyers is there’s loads of worth outdoors of the mega-cap shares. Valuations for small and mid cap shares are nonetheless fairly low cost. They’re far cheaper now than they had been earlier than the pandemic. Possibly there’s a cause for that however shares don’t get low cost for no cause.

Valuations haven’t mattered that a lot throughout this prolonged bull market as a result of the largest, fastest-growing firms have been so dominant. It’s doable that might proceed. So long as earnings proceed to develop it appears silly to wager towards the most effective firms on this planet.

Nevertheless, there are cheaper areas of the market should you’re involved about valuations.

Diversification goes to show its price once more sooner or later. I simply don’t know when.

Michael and I talked about inventory market valuations and rather more on this week’s Animal Spirits video:

Subscribe to The Compound so that you by no means miss an episode.

Additional Studying:

Timing the Inventory Market Utilizing Valuations

Now right here’s what I’ve been studying these days:

Books:

1Many buyers assume the explanation shares took off as a result of the election consequence got here so rapidly. I can see that.

2A number of the numbers in these charts are trailing 12 month PE ratios and a few are ahead PE ratios. That’s why the numbers don’t all the time match up completely. Shut sufficient is sweet sufficient for valuations.

This content material, which incorporates security-related opinions and/or info, is supplied for informational functions solely and shouldn’t be relied upon in any method as skilled recommendation, or an endorsement of any practices, services or products. There might be no ensures or assurances that the views expressed right here will likely be relevant for any explicit info or circumstances, and shouldn’t be relied upon in any method. It’s best to seek the advice of your individual advisers as to authorized, enterprise, tax, and different associated issues regarding any funding.

The commentary on this “publish” (together with any associated weblog, podcasts, movies, and social media) displays the non-public opinions, viewpoints, and analyses of the Ritholtz Wealth Administration workers offering such feedback, and shouldn’t be regarded the views of Ritholtz Wealth Administration LLC. or its respective associates or as an outline of advisory companies supplied by Ritholtz Wealth Administration or efficiency returns of any Ritholtz Wealth Administration Investments shopper.

References to any securities or digital belongings, or efficiency information, are for illustrative functions solely and don’t represent an funding suggestion or provide to offer funding advisory companies. Charts and graphs supplied inside are for informational functions solely and shouldn’t be relied upon when making any funding resolution. Previous efficiency is just not indicative of future outcomes. The content material speaks solely as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these supplies are topic to vary with out discover and should differ or be opposite to opinions expressed by others.

The Compound Media, Inc., an affiliate of Ritholtz Wealth Administration, receives fee from numerous entities for commercials in affiliated podcasts, blogs and emails. Inclusion of such commercials doesn’t represent or indicate endorsement, sponsorship or suggestion thereof, or any affiliation therewith, by the Content material Creator or by Ritholtz Wealth Administration or any of its workers. Investments in securities contain the danger of loss. For added commercial disclaimers see right here: https://www.ritholtzwealth.com/advertising-disclaimers

Please see disclosures right here.