{kind=link}

In early September, CHIR Assistant Analysis Professor Christine Monahan testified earlier than the Texas Home Insurance coverage Committee on outpatient facility charge billing and potential reforms. The Texas legislature is at present making ready for its 89th legislative session subsequent spring, and the current listening to will play a vital function in shaping laws to return.

Christine’s feedback to the committee observe. A corresponding slide deck is out there right here.

At CHIR, we examine non-public medical health insurance and well being care markets, conduct authorized and coverage evaluation, and supply technical help to federal and state policymakers, regulators and stakeholders on a spread of matters. With the assist of West Well being, I and a number of other members of the CHIR crew have been learning outpatient facility charge billing for the previous two years. We’ve performed a number of dozen interviews with on the bottom stakeholders, reviewed present legal guidelines and pending laws at each the state and federal ranges, written a number of analyses, and, most just lately, printed a set of maps reporting on our evaluate of the legal guidelines in all 50 states and the District of Columbia associated to outpatient facility charge billing.

Step one to understanding facility charge billing is to know that there are two forms of claims sometimes used to invoice for medical companies: an expert invoice (the CMS-1500) and the power invoice (the UB-04). In the event you obtain care at an unbiased supplier apply, the supplier who handled you’ll submit an expert invoice to your insurer. This invoice, in concept, covers their time and labor in addition to any apply overhead prices, like nursing workers, lease, and gear and provides. Then again, when you obtain care at a hospital outpatient division, usually talking any skilled who handled you, in addition to the hospital, will every submit separate payments. Any skilled payments ought to simply cowl the supplier’s time and labor, whereas the hospital invoice – or facility charge – ostensibly covers overhead prices.

What counts as hospital overhead and what else goes right into a facility charge is sophisticated, nevertheless. As you’d count on, a facility charge usually will cowl the overhead prices associated to the affected person go to for which it’s being billed, together with the nurses or assist workers concerned and any gear and provides. As a result of hospital outpatient departments want to satisfy additional licensure and regulatory necessities, they seemingly even have some further prices that don’t apply to unbiased settings.

As well as, a facility charge is prone to cowl different hospital overhead prices. A few of these are needed and fascinating companies on the inhabitants degree, however not associated to the care delivered to the affected person who’s getting billed. For instance, facility charges would possibly assist fund issues like hospital emergency companies, or 24/7 staffing and safety on the hospital, regardless that the affected person was on the facility throughout regular enterprise hours and didn’t want any emergency care or they went to a very separate, off-campus facility ten miles from the hospital campus and emergency room. Hospital overhead prices may embody issues of extra debatable worth – from excessive CEO salaries, to costly paintings or gourmand meals companies, to, I child you not, film manufacturing studios. All of this stuff could also be thought-about hospital “prices” that sufferers may be requested to pay by way of a facility charge.

It is usually necessary to know that different components, unrelated to the price of care or different bills a hospital has, additionally play a giant function in figuring out how a lot a hospital payments for and will get paid by insurers, together with historic billing patterns and market energy. Notably as hospitals and well being programs get greater, and vertically combine, they’ve rather more energy than your solo doctor or unbiased group apply to demand increased reimbursement when negotiating with insurers.

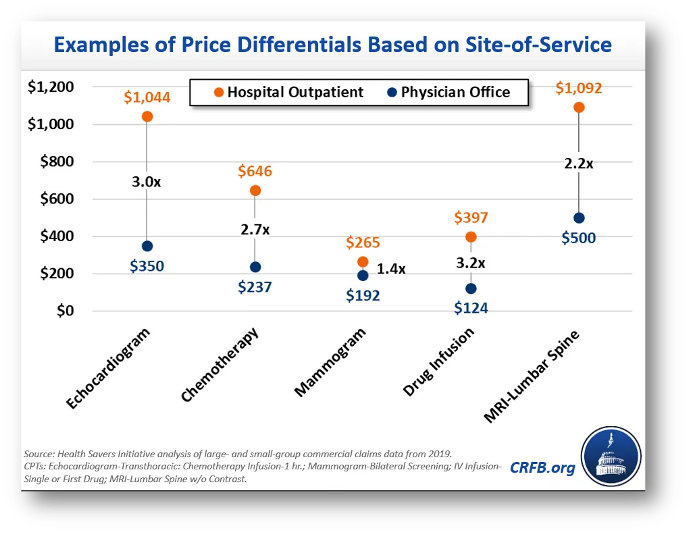

So, when financial consultants evaluate the costs paid for a similar companies at hospital outpatient departments and unbiased doctor places of work, they discover a lot increased costs in hospital settings. Chemotherapy is one instance from the Committee for a Accountable Federal Funds. A affected person going for weekly chemotherapy visits would see, on common, a 2.7-fold distinction in value in the event that they switched from an unbiased apply to a hospital outpatient division. And, in fact, they’re typically not those making that alternative to change – somewhat, someday in the course of remedy they might go into the identical workplace constructing as at all times, for a similar care as at all times, and are available away with a invoice that’s greater than $400 increased than what they’re used to as a result of a hospital acquired their apply and transformed it to a hospital outpatient division.

It’s this current historical past of aggressive hospital acquisition of outpatient practices that’s driving the difficulty at this time. Facility charge billing just isn’t a novel apply, however it’s extra widespread than it was once following years of vertical integration the place hospitals are buying or constructing their very own outpatient doctor practices and clinics. Certainly, one of many causes hospitals and well being programs have considerably expanded their possession and management over outpatient doctor practices over the previous decade or so, is so they may cost this second invoice and improve their revenues.

One other seemingly purpose we’re listening to about facility charge billing extra now are inadequacies in insurance coverage protection. Because the hospital business will emphasize, sufferers more and more are coming in with excessive deductible well being plans which depart them uncovered to extra expenses, together with facility charges. The hospitals should not fallacious in declaring this hole, however it’s best understood as a symptom of the higher drawback of rising costs.

Larger spending on outpatient care from facility charge expenses is growing the price of medical health insurance for all of us: sufferers and shoppers who enroll in medical health insurance, employers who’re sponsoring insurance coverage for his or her employees and paying greater than 70-80% of their well being plan premiums, and taxpayers who closely subsidize the non-public medical health insurance market. Economist Stephen Parente, who served on the White Home Council of Financial Advisers within the Trump Administration, just lately launched a examine discovering that employer plan premiums may go down greater than 5% yearly if insurers paid the identical quantity for care in a hospital outpatient division as they do an unbiased doctor’s workplace. This in flip would end in $140 billion in financial savings to the federal authorities over ten years by way of decreased tax subsidies for employer plans. Whereas not the one issue, outpatient facility charge billing is contributing to the rising unaffordability of medical health insurance at this time.

On the similar time, insurers are responding to those value will increase largely by growing cost-sharing and in any other case limiting advantages. Because the hospital business factors out, medical health insurance deductibles are growing in measurement and prevalence. Lots of these $200, $300, $400+ facility charges are going straight to the affected person. Customers can also face increased cost-sharing for care offered at a hospital outpatient division even when their deductible doesn’t apply. This may be as a result of the power charge is carrying its personal distinct cost-sharing obligation from the skilled invoice or as a result of insurers set increased cost-sharing charges for companies offered at hospital outpatient departments to attempt to discourage sufferers from going to them. Moreover, some insurers could merely not cowl a service when it’s offered at a hospital outpatient division, in an effort to comprise their very own spending whereas doubtlessly opening up sufferers to stability billing.

In sum, inadequacies in insurance coverage protection are enjoying a job in exposing shoppers to excessive medical payments which is driving media consideration. But when insurance coverage coated these expenses with none cost-sharing, shoppers in addition to employers and taxpayers would nonetheless be paying for it by way of their premium {dollars} – it simply could be much less seen.

What, then, may be accomplished to deal with these issues? One possibility is to proceed to attend to see if the non-public market will repair it. However there are obstacles to personal reforms, together with a lack of understanding, an absence of leverage, and an absence of motivation.

With respect to data, one of many refrains we constantly hear from stakeholders is that there are important gaps in claims knowledge that make it difficult for personal payers and regulators alike to know the complete scope and influence of facility charge billing. Particularly, they reported that it may be very tough if not unattainable to establish the precise brick and mortar location the place care was offered on a claims kind or in a claims database. The handle line may discuss with the primary campus of a hospital that owns the apply, and even an out-of-state billing workplace for the well being system.

By way of leverage, dominant hospitals often have the upper-hand in negotiations with insurance coverage firms as a key promoting level for insurers is that they’ve the identify model hospital or doctor group of their community. In Massachusetts, one of many main insurers proactively sought to get rid of outpatient facility charge billing by in-network suppliers, however may solely do that in a finances impartial method (agreeing to lift charges elsewhere to make up the distinction) and nonetheless one main well being system has refused to play ball and continues to invoice facility charges at this time. Reforms like prohibiting anticompetitive contracting clauses, as Texas has enacted, could start to chip away at components contributing to hospitals’ dominance in negotiations nevertheless.

Relating to motivation, insurers usually don’t profit from decreasing well being care prices as they take dwelling a proportion of spending. However public scrutiny on egregious facility charges in Massachusetts motivated the insurer I beforehand talked about to behave, and will encourage different insurers elsewhere to observe go well with. Moreover, giant employers more and more are partaking on this and different well being care spending points, and they are able to strain insurers to get rid of facility charge billing of their contracts with suppliers. Certainly, I do know of at the very least two state worker well being plans which have accomplished so.

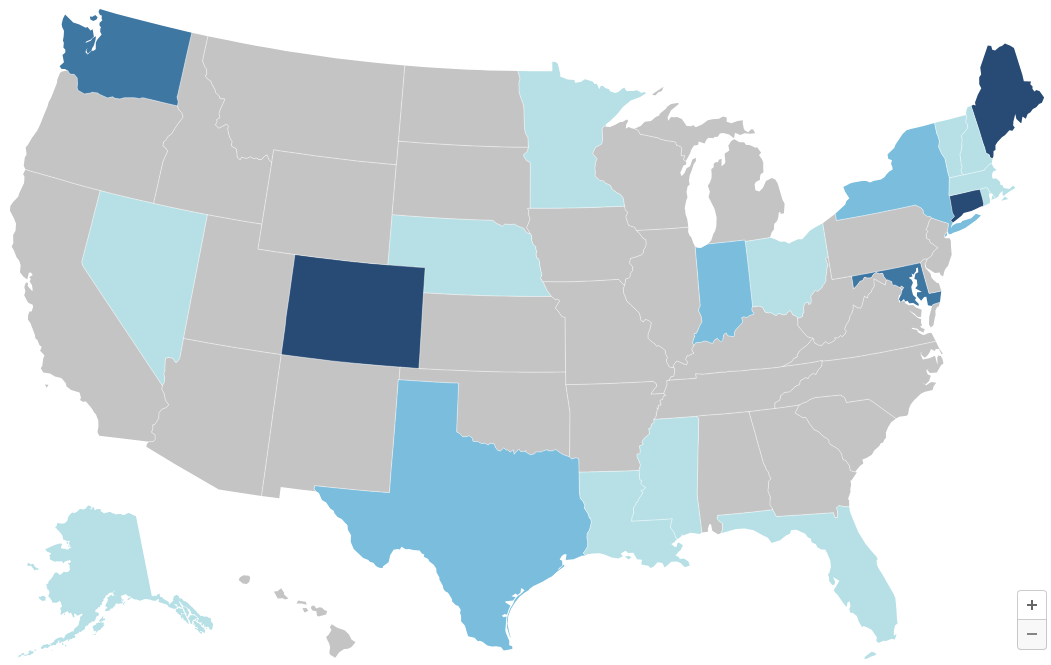

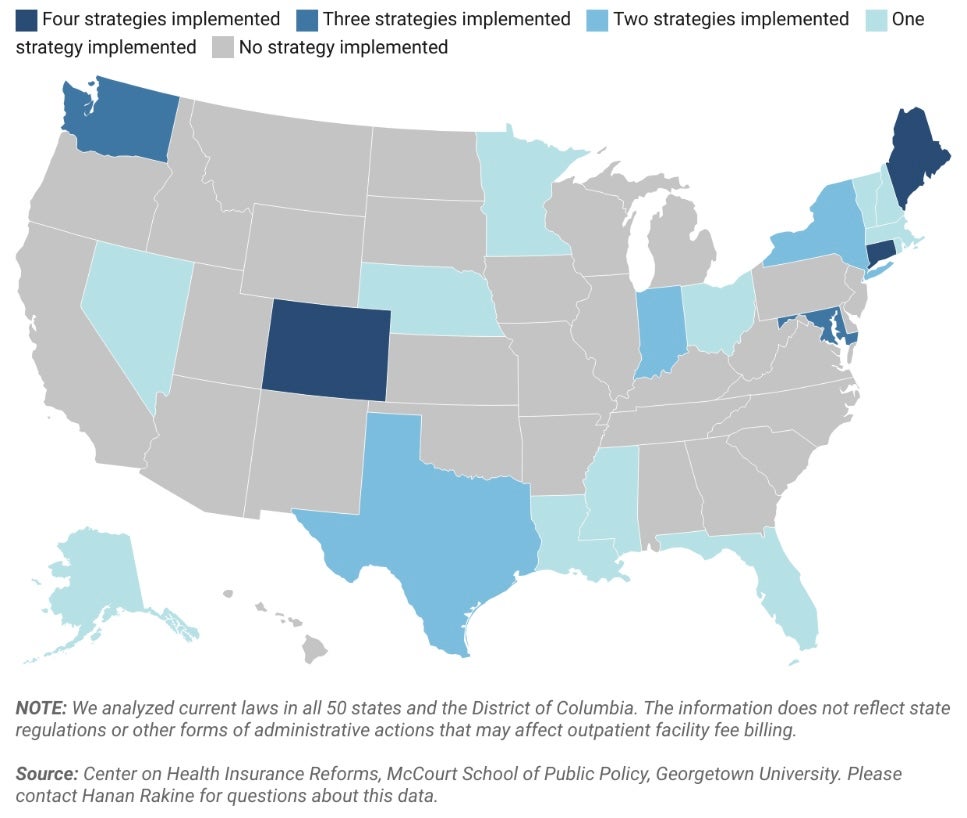

In the end, although, facility charge billing and different aggressive hospital pricing and billing practices are an uphill battle for the non-public market to sort out alone. Accordingly, we’re seeing states throughout the nation, reflecting broad geographic and political range, start to pursue legislative reforms. By our depend, twenty states nationwide have enacted a number of of the six potential options our crew has recognized: web site impartial fee reforms, facility charge billing bans, billing transparency necessities, public reporting necessities, cost-sharing protections, and client notification necessities. I’m going to concentrate on simply the primary three I discussed proper now, however now we have further data on others and I’m glad to debate any of them. Importantly, none of those reforms are mutually unique. They merely sort out the problems from completely different, however complementary angles.

First, states are starting to sort out the transparency points I simply raised. Notably Colorado, Nebraska, and Nevada now require off-campus hospital outpatient departments to amass a novel, location-specific supplier identifier quantity – generally known as an NPI – and embody it on claims types. This can be a easy and minimally burdensome reform that will enormously improve claims knowledge. As Colorado has discovered, pairing this knowledge with a system for monitoring which NPI belongs to which well being system could make it much more helpful, as it might give visibility into each the situation of care and who owns that setting. This data may assist non-public payers or regulators and policymakers rein in outpatient facility charge billing. It additionally may very well be useful in serving to payers undertake tiered supplier networks or in any other case steer sufferers in the direction of or away from completely different supplier areas primarily based on the standard or value of care they supply.

A state looking for to go additional than that might prohibit hospital outpatient departments from charging facility charges for specified companies. Texas, in fact, has already accomplished this very narrowly for companies like Covid-19 assessments and vaccinations when carried out at drive-through clinics at free-standing emergency departments. States like Connecticut, Maine, and Indiana, nevertheless, have extra broadly prohibited hospitals and well being programs from charging facility charges for outpatient analysis and administration companies or different office-based care in sure settings.

By prohibiting facility charges for specified companies, policymakers shield sufferers from doubtlessly bearing the cost-sharing brunt of two payments. For instance, somewhat than owing a $30 copay on the doctor’s invoice and a 40% coinsurance cost on the power charge, the affected person will return to owing only a $30 copay, as if they’d obtained care in an unbiased setting. For the massive proportion of the inhabitants who don’t have sufficient money to pay typical non-public plan cost-sharing quantities, it is a actually huge deal. On the similar time, the system-wide financial savings from such a reform seemingly might be comparatively muted in the long run, as market highly effective hospitals renegotiate their contracts and improve different costs to make up for the lack of income from facility charges, as we noticed occur in Massachusetts.

Lastly, policymakers who’re feeling notably formidable could need to take into account site-neutral fee reforms, which is what Stephen Parente was learning. These reforms name for insurers to pay the identical quantity for a similar service, no matter whether or not the service was offered at a hospital outpatient division or an unbiased apply.

How this works, and the way huge of an impact it might have, rely upon numerous design selections. As with facility charge bans, one of many vital selections might be what companies are coated and this may very well be broad or slim. Simply as necessary is who determines how a lot insurers pay for a service and the way this fee degree compares to present costs. Below essentially the most hands-off model of a site-neutral coverage, lawmakers may merely require that insurers undertake site-neutral funds with out specifying a fee degree and leaving that to personal market negotiations. Alternatively, lawmakers may establish, or activity regulators with figuring out, a benchmark degree be it tied to present business charges or a public charge schedule, equivalent to a proportion of Medicare. The extra companies coated and the decrease the fee degree, the higher the financial savings.

No state at this level has enacted a site-neutral coverage within the business sector up to now, however there may be rising curiosity and I anticipate that we are going to see some site-neutral payments launched within the coming yr.

Thanks for having me.