{kind=link}

A reader asks:

I believe the schooling of retail buyers is healthier than it’s ever been — blogs, books, newsletters, podcasts, and many others. The correct schooling about how loopy markets are and to not overreact and to suppose long-term is working. And that’s why retail is the good cash now. Could possibly be a great subject: Is monetary schooling working?

My quick reply is, sure, monetary schooling appears to be working.

Permit me to elucidate.

After I graduated faculty and began my first job I shortly realized I had a bunch of textbook data however no understanding of how markets, folks, incentives, habits or investing works in the actual world.

This was again in 2005.

There have been no podcasts, blogs, newsletters, YouTube channels or social media personalities to be taught from. So I learn as many books concerning the markets and behavioral psychology as I might get my fingers on.

I peppered folks with questions. My boss was form sufficient to offer me a tutorial on a whiteboard each few weeks about how the markets work. He taught me about asset allocation, diversification, funding coverage, and the right way to talk with shoppers.

It definitely wasn’t simple and took various years till I used to be comfy sufficient to really feel like I knew something of substance.

Investing itself was troublesome too.

There have been larger minimums, larger charges, no zero-trade commissions, much less automation and a bunch of antiquated legacy monetary corporations that usually made it troublesome to speculate when you had been simply beginning out.

Now we now have significantly better assets. The boundaries to entry have vanished. Now you can arrange an account in your iPhone and purchase fractional shares of shares 5 minutes later. Plus, buyers have been overwhelmed over the top for 15 years straight concerning the energy of long-term pondering, market timing is difficult, don’t panic, and many others.

Within the outdated days, the idea was that retail buyers would purchase excessive and promote low. They acquired grasping when others had been grasping and fearful when others had been fearful.

That’s not the case anymore.

The dumb cash isn’t so dumb anymore.

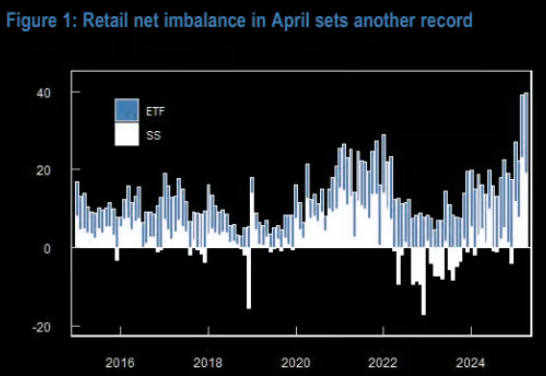

JP Morgan knowledge reveals there was a file month-to-month influx by retail buyers in April to the tune of $40 billion:

The inventory market fell 20% and retail buyers didn’t run for the exits. They purchased low!

Markets had been in a freefall and retail was the regular hand. How about Wall Road?

In accordance with Barron’s, skilled buyers had been extra bearish on shares than they’ve been in no less than 30 years.

The good cash acquired scared. The dumb cash rushed into the burning constructing. Possibly the good cash isn’t so good anymore.

After all, being a great long-term investor is not only about shopping for shares after they’re down (though it helps).

There are actually extra set-it-and-forget-it buyers than ever earlier than.

In 2024 simply 5% of buyers in a Vanguard 401k plan made modifications to their portfolio. There may be now greater than $4 trillion in targetdate funds. Extra money goes into index funds and ETFs and out of actively managed funds:

Buyers are making higher choices than ever earlier than.

Does this imply retail buyers are good?

After all not!

There are nonetheless loads of individuals who speculate, make use of an excessive amount of leverage, chase fads, commerce short-dated choices and spend money on stuff they don’t perceive.

However that’s all the time going to be the case. You may’t save everybody. If everybody had been a disciplined long-term investor, long-term investing wouldn’t work in addition to it does.

I’ve been utilizing the phrases good and dumb cash lots right here however I’m not an enormous fan of that nomenclature. There are clever skilled buyers. There are clever retail buyers. There are silly skilled and retail buyers too.

I don’t know who the good cash is precisely. It appears to alter from cycle to cycle.

However retail as an entire is definitely not the dumb cash anymore.

Monetary schooling is working and investor habits is bettering.

It is a fantastic improvement.

Steve Quirk from Robinhood joined me on Ask the Compound this week to cowl this query in larger element:

We additionally mentioned why buyers are shopping for the dip extra typically, the way forward for retail buying and selling, how tax-deferred retirement accounts will evolve and the way AI will change the wealth administration panorama.

Additional Studying:

Two of the Greatest Traits This Decade